7 Common Annuity Myths (And What the Contracts Actually Say)

If you have researched retirement planning for more than five minutes, you have probably heard some scary things about annuities.

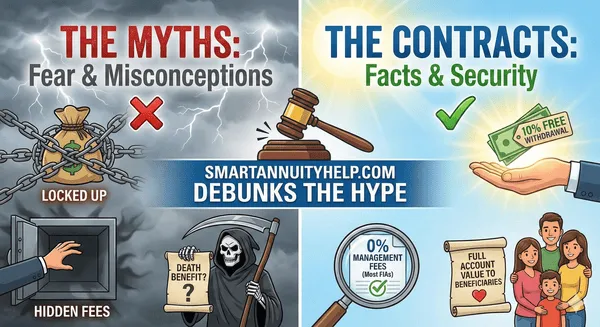

You might have heard that they are expensive, that they lock up your money forever, or—the biggest fear of all—that the insurance company keeps your money when you die.

Here is the truth: Some annuities are bad. We agree! There are types of annuities (specifically Variable Annuities) that are often loaded with high fees and market risk. We generally tell our clients to avoid them.

However, painting all annuities with that same brush is like saying "all food is bad for you" because you ate a stale donut once.

At SmartAnnuityHelp.com, we believe in facts, not fear. Let’s look at the actual contracts of modern Fixed Index Annuities (FIAs) and debunk the 7 biggest myths.

Myth #1: "The Insurance Company Keeps My Money When I Die"

The Reality: This is the most pervasive myth, and for most modern annuities, it is 100% false. This myth comes from old-school "Immediate Annuities" where you traded a lump sum for a paycheck, and if you died a year later, the money was gone. The Contract Fact: With a Fixed Index Annuity, your account has a cash value. If you pass away, 100% of that accumulation value passes directly to your beneficiaries, usually avoiding probate. Your family gets the money, not the insurance company.

Myth #2: "Annuities Have Hidden Fees That Eat Your Profit"

The Reality: This is true for Variable Annuities (which can have fees of 3-4% per year). The Contract Fact: Most Fixed Index Annuities have $0 in annual management fees. The insurance company makes its money on the "spread" (the difference between what they earn and what they pay you), not by charging your account. Note: If you choose to add an optional "Income Rider" for guaranteed lifetime pay, there is usually a small fee (often roughly 1%), but you are receiving a specific benefit for that cost.

Myth #3: "I Will Lose Access to My Money (Liquidity)"

The Reality: People think putting money in an annuity is like locking it in a vault you can't open for 10 years. The Contract Fact: Almost all contracts allow you to withdraw 10% of your account value every single year, penalty-free. Need $20,000 for a roof repair or a medical emergency? It is there for you.

Myth #4: "The Returns Are Terrible"

The Reality: Critics say annuities don't perform as well as the S&P 500. The Contract Fact: They aren't supposed to beat the S&P 500! They are designed to beat CDs and Bonds while eliminating the risk of crashing. If the market does 10%, you might get 6-7%. But if the market does -20%, you get 0%. It is a safety tool, not a speculative tool.

Myth #5: "Once I Buy It, I Can Never Change It"

The Reality: Many people fear "Surrender Charges." The Contract Fact: While annuities are long-term vehicles, surrender charges decrease over time (usually over 5, 7, or 10 years). Once that term is over, your money is completely liquid. You are not "stuck" forever; you are just committing to a term, similar to a CD, in exchange for protection.

Myth #6: "Annuities Are Only for People Who Are Bad at Investing"

The Reality: Some think annuities are for the unsophisticated. The Contract Fact: Some of the wealthiest people in the world use annuities. Why? Because the wealthy don't care about "hitting a home run" with every dollar. They care about staying wealthy. They use annuities to ring-fence their essential income so they can take risks with the rest of their portfolio.

Myth #7: "My Financial Advisor Says They Are Bad"

The Reality: Many advisors work for firms that incentivize them to keep your money in the stock market (where they charge an ongoing 1% fee on your total assets). The Contract Fact: If you move money into an annuity, that advisor loses their 1% fee on that money. It is a conflict of interest that few will admit to. Ask your advisor: "If the market crashes 30% next year, do you still charge your fee?" (The answer is yes).

Get the Facts, Not the Hype

Retirement is too important to base your decisions on outdated myths. You need to see the actual numbers, the actual contracts, and how they apply to your specific situation.

To learn more about how these concepts can fit in your retirement, schedule a time below.

Book Your Complimentary Strategy Call with a SmartAnnuityHelp Expert